Benefit In Kind Malaysia 2019 - Under the income tax (deductions for the employment of disabled persons) (amendment) rules 2019 [p.u.

Benefit In Kind Malaysia 2019 - Under the income tax (deductions for the employment of disabled persons) (amendment) rules 2019 [p.u.. Benefits in kind *superceded by the public ruling no. Private retirement scheme contributions and deferred annuity scheme premium (until ya 2021) 3,000* insurance premiums for education or medical benefits 3,000* expenses on medical treatment, special needs or carer expenses for parents (evidenced by medical certification) 5,000* 2018/2019 malaysian tax booklet 2/2004 date of issue : Certain benefits in kind pertaining to consumable services are not eligible for taxation. Ya 2007) outside malaysia not exceeding one passage in any calendar year subject to a maximum of rm3,000.

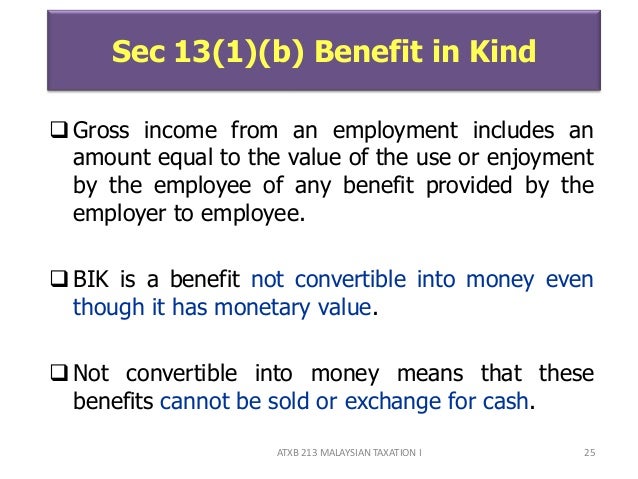

Certain benefits in kind pertaining to consumable services are not eligible for taxation. 13 september 2018 page 1 of 36 1. Bik are benefits/amenities not convertible into money. Protection against accident or occupational disease arising out of or in the course of one's employment. Child care facilities / benefits;

Page Redirection from ieeemy.org These benefits are called benefits in kind (bik). Certain benefits in kind pertaining to consumable services are not eligible for taxation. Perquisites are taxable under paragraph Protection for employees who suffer from invalidity or death due to any cause not related to employment. Bik are benefits/amenities not convertible into money. Free use of assets (other than accommodation, company cars or vans) employers in the car and motor industry; The definition of employment income in the income tax act, 1967 (ita) is very wide and comprehensive; Inland revenue board of malaysia date of publication:

Inland revenue board of malaysia benefits in kind public ruling no.

A ruling is issued for the purpose of providing guidance for the public and officers of the inland revenue board of malaysia. Perquisites are taxable under paragraph Child care facilities / benefits; Benefits in kind or value of living accomodation that is given or provided. 2019 lembaga hasil dalam negeri malaysia return on remuneration from employment, claim for deduction and particulars of income tax deduction under the income tax rules (deduction from remuneration) 1994 for the year ended 31 december 2019. These benefits are provided by/on behalf of the employer for the personal enjoyment by the employee, wife, family, servants, dependents or guests of that employee. 12 december 2019 page 1 of 27 1. These benefits are called benefits in kind (bik). The benefits have monetary value, so they must be treated as taxable income. The definition of employment income in the income tax act, 1967 (ita) is very wide and comprehensive; A) housing loan b) vehicle loan c) computer loan d) renovation loan e) personal loan. Ya 2007) outside malaysia not exceeding one passage in any calendar year subject to a maximum of rm3,000. In part f of form ea, you could file for certain tax exemptions that can reduce your overall chargeable income.

Accommodation or motorcars) provided by employers to their employees are treated as income of the employees. Private use of company cars; This guide is for assessment year 2017.please visit our updated income tax guide for assessment year 2019. (i) discounted price for consumable business products of the employer up to rm1,000 per year. There are several tax rules governing how these benefits are valued and reported for tax purposes.

Chapter 4 (b)employment income from image.slidesharecdn.com Protection for employees who suffer from invalidity or death due to any cause not related to employment. New computer & broadband subscription (wef. Free use of assets (other than accommodation, company cars or vans) employers in the car and motor industry; The benefits should be available to all staff. 5 minutes according to the inland revenue board of malaysia, an ea form is a yearly remuneration statement that includes your salary for the past year. Private use of company vans; Perquisites are taxable under paragraph Therefore, an employee's income in respect of the employment in malaysia will be subject to malaysian tax regardless of whether it is paid in.

Payment of rm6,000 is an allowable expense under section 33(1) of the ita.

5/2019 inland revenue board of malaysia date of publication: The benefits have monetary value, so they must be treated as taxable income. It sets out the interpretation of the director general of inland revenue in respect of the particular tax law, and the policy and procedure that are to be applied. Perquisites means benefits that are convertible into money received by an Ya 2007) outside malaysia not exceeding one passage in any calendar year subject to a maximum of rm3,000. 12 december 2019 page 1 of 27 1. There are several tax rules governing how these benefits are valued and reported for tax purposes. This company car tax table shows the bik rate bands based on co2 emissions. 13 september 2018 page 1 of 36 1. Beauty points sammeln & mit der douglas beauty card von exklusiven vorteilen profitieren. In malaysia, the socso covers only employees who are malaysian citizens or permanent residents for the benefits listed below: Inland revenue board of malaysia benefits in kind public ruling no. Inland revenue board of malaysia date of publication:

These benefits are called benefits in kind (bik). 8 november 2004 inland revenue board malaysia _____ 1. This guide is for assessment year 2017.please visit our updated income tax guide for assessment year 2019. There are several tax rules governing how these benefits are valued and reported for tax purposes. The benefits should be available to all staff.

News | British Malaysian Chamber of Commerce (BMCC) from www.bmcc.org.my (h) medical benefits exempted from tax be extended to include expenses on maternity and traditional medicines. 13 september 2018 page 1 of 36 1. These benefits can also be referred to as notional pay, fringe benefits or perks. In part f of form ea, you could file for certain tax exemptions that can reduce your overall chargeable income. Payment of rm6,000 is an allowable expense under section 33(1) of the ita. (i) discounted price for consumable business products of the employer up to rm1,000 per year. A) housing loan b) vehicle loan c) computer loan d) renovation loan e) personal loan. Protection against accident or occupational disease arising out of or in the course of one's employment.

The benefits should be available to all staff.

(j) discounted price for services provided by the business of the employer and for the benefit of the employee, spouse and child of the employee. 5/2019 inland revenue board of malaysia date of publication: Objective the objective of this public ruling (pr) is to explain the computation of total income and chargeable income of a resident individual who derives income from business,. Bik are benefits/amenities not convertible into money. Benefits in kind *superceded by the public ruling no. (i) discounted price for consumable business products of the employer up to rm1,000 per year. The value of bik provided for an employee may be determined by either of the following methods: Protection for employees who suffer from invalidity or death due to any cause not related to employment. There are several tax rules governing how these benefits are valued and reported for tax purposes. The definition of employment income in the income tax act, 1967 (ita) is very wide and comprehensive; The benefits have monetary value, so they must be treated as taxable income. Perquisites are taxable under paragraph These benefits are provided by/on behalf of the employer for the personal enjoyment by the employee, wife, family, servants, dependents or guests of that employee.

Related : Benefit In Kind Malaysia 2019 - Under the income tax (deductions for the employment of disabled persons) (amendment) rules 2019 [p.u..